Are Insurance Proceeds Taxable?

In the aftermath of loss or disaster, taxes are the last thing you want to consider. However, being tax-compliant is necessary. Understanding the tax implications of your insurance proceeds is vital to help you navigate financial matters successfully after unforeseen events. These implications can vary depending on the nature of your claim, insurance type, and local tax regulations.

Identifying Types of Insurance Proceeds

Insurance proceeds are the funds or payments resulting from a covered claim or event. These include various scenarios, including life insurance benefits, health insurance reimbursements, casualty claims, and property settlements. Each scenario can take different forms. For example, you may receive proceeds from a property insurance claim for repairs or to replace a severely damaged property. Proceeds from various types of insurance settlements may include:

- Life insurance proceeds: Life insurance gives beneficiaries a death benefit to cover income gaps after losing a loved one.

- Disability insurance proceeds: The settlement from disability insurance serves as income replacement.

- Health insurance proceeds: These proceeds cover your medical expenses, which include surgeries, hospital stays, and prescription medication.

- Property insurance proceeds: Property insurance helps cover property damage or loss and includes homeowners or renters insurance.

- Business insurance proceeds: Much of this insurance type aims to cover a temporary loss of profit.

Life Insurance Proceeds

Both term and permanent life insurance proceeds are not classified as gross income, so beneficiaries are not obligated to report them. However, if the policyholder receives their death benefits while they are alive, like with a settlement, they may be liable to pay taxes. The interest you receive from these proceeds is also taxable, and how you will report this depends on the type of income document you receive.

Large estates may trigger federal or state estate taxes. For estate tax purposes, the life insurance proceeds often form part of the deceased person’s estate in these cases. This may change the nature of the payment and can trigger taxation.

Disability Insurance Proceeds

The proceeds from your disability insurance replace a portion of your income if you cannot fulfill employment obligations. Taxation depends on whether you paid premiums using your pre-tax or after-tax dollars. Regardless, you must report all proceeds from disability insurance as income. If your employer pays you when you are ill or injured, this forms part of your income.

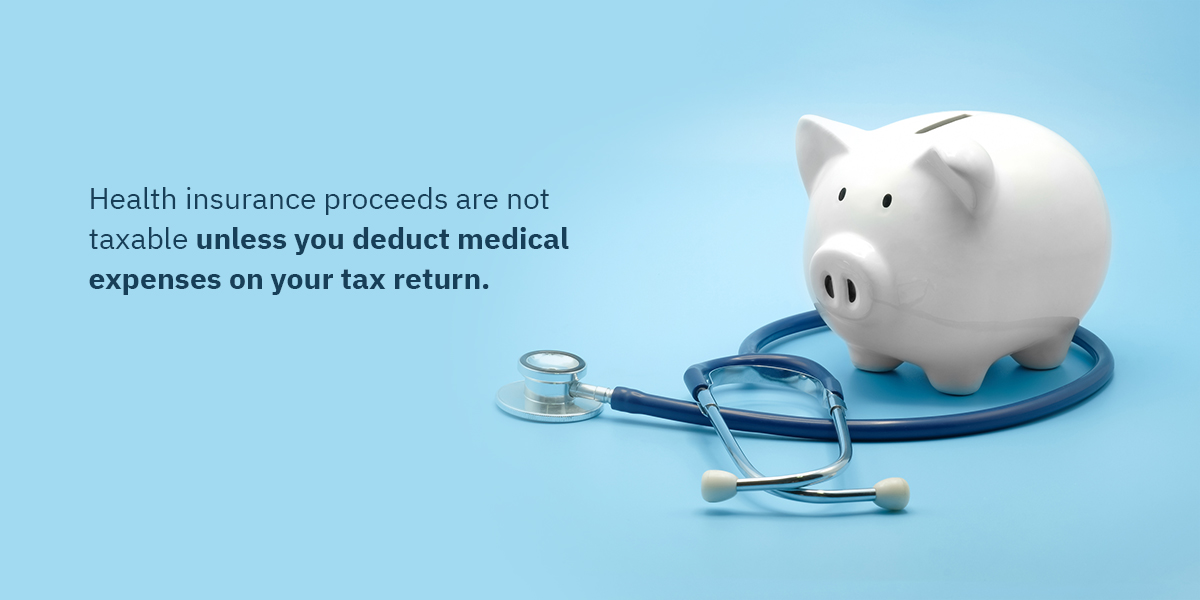

Health Insurance Proceeds

Health insurance proceeds are not taxable unless you deduct medical expenses on your tax return. Receiving an insurance reimbursement for these expenses can invoke tax implications, whether you are on private or employer-sponsored health plans. The benefits you receive from long-term care insurance policies may be subject to certain conditions and limitations, but they are not taxable. Keeping records of all your insurance reimbursements and medical expenses for tax purposes may support your case to avoid taxation.

Property Insurance Proceeds

The Internal Revenue Service (IRS) excludes settlements for property loss or value from taxable incomes. The result is that insurance proceeds for property damage are not taxable unless the settlement includes compensation for punitive damages or emotional distress. You must report these as “other income” on Schedule 1, line 8z on Form 1040, under “Additional Income and Adjustments.”

Another exception is if the settlement you get exceeds the restoration cost, which classifies the proceeds as capital gains, opening it up to taxation. If you get a Form 1099 for your insurance proceeds, review the form to establish if it is accurate. Contact the issuer to correct any errors or discrepancies.

Business Insurance Proceeds

Your business insurance shields you against personal injury lawsuits and business losses like property damage. As long as the reimbursement you get from filing an insurance claim does not surpass the value of the loss, insurance proceeds are not taxable to a business. Casualty loss insurance proceeds for business property damage are not taxable either. If your insurance fails to cover the loss, you can likely deduct the loss against your business income.

Here are some other types of business insurance proceeds and whether you can claim them tax-free:

- Business interruption insurance: This insurance compensates for lost income and is often considered taxable income.

- Key person life insurance: When your business is the beneficiary of a key person life insurance policy, the proceeds are tax-free. However, the policy structure or other circumstances may change the nature of this settlement to see it as an income.

- Liability insurance: If the proceeds of your liability insurance compensate for a loss, it is often deductible as a business expense. As a result, those proceeds may be taxable.

- Employee benefits: In many cases, the insurance benefits for your employees are tax-deductible, and the employees receive these benefits tax-free.

How to Tell if Your Insurance Proceeds Are Taxable

Several general principles influence the potential taxation of your insurance proceeds. Keep all documents from your insurance company for your records, even if the proceeds are not taxable. Consult a professional to clarify whether you must file insurance proceeds with your income taxes.

- Capital vs. income: Generally, you can distinguish taxation based on capital versus income replacement. Insurance proceeds that replace lost income may be subject to income tax. Proceeds resulting from the capital loss, like property insurance payouts for damage, may not be subject to taxation.

- Deductibility and premiums: The premiums you pay for personal insurance, like disability, health, or life insurance, with your after-tax dollars will usually be tax-free. However, those you pay for with after-tax dollars, like employer-sponsored plans, may result in taxation.

- Legal judgment: If you receive proceeds resulting from legal judgments or settlements, these may also be liable for taxation. Factors that may impact this include the nature of your claim and whether it involves emotional distress or personal injury.

Manage Your Insurance Proceeds With Fort Pitt Capital Group

You can optimize your financial outcomes by understanding how your payout fits the relevant tax laws. You will also need to follow some specific accounting procedures, including the total amount of the proceeds and loss. Getting advice from a knowledgeable financial advisor and investment strategist on allocating your insurance proceeds ensures you prioritize your wealth preservation.

The knowledgeable team at Fort Pitt Capital Group can help. Our financial services include wealth management, insurance advisory, investment consulting, and more. For more information about our financial planning and portfolio management services, contact us online today, or call us at 1-800-471-5827.