How Much House Can You Afford?

If you’re looking to buy a house, you first need to consider your budget and how much you can realistically afford to pay for your mortgage. Before putting your information into a mortgage calculator, take a moment to understand how a lender will determine your mortgage and some alternative loans for which you may be eligible.

What Factors Help Determine How Much House You Can Afford?

A potential lender will look at your finances to determine if you will be a good candidate for their loan. Expect them to request information on your household income, debts, and savings. Before this review, we suggest you have about three months worth of any payments you regularly make in your savings.

The most important factor banks and other lenders use to determine if you qualify for a mortgage loan is your debt-to-income, or DTI, ratio. Your DTI ratio compares your debt to your gross income. The percentage of monthly income spent on monthly debts is your DTI. There are two types of DTI:

- Back-end DTI considers all monthly debts, including student and automobile loans. Your back-end DTI should be less than 43% to receive a qualified mortgage.

- Front-end DTI examines only your debts related to housing. Lenders want to see a front-end DTI of 28% or less for mortgage applications.

Alternative Loans

Many people have trouble getting approved for a conventional loan for various reasons. However, some special loans give potential buyers other available options on the path to homeownership.

- FHA loans: The Federal Housing Administration insures an FHA mortgage loan. FHA loans allow people with low credit scores or little savings to get a mortgage that a conventional loan might not cover. Down payments start at just 3.5%, and you can still get approval with a DTI of up to 50%.

- VA loans: This loan type is a mortgage loan insured by the U.S. Department of Veteran Affairs. It covers primary residences that are in “move-in ready” condition. The main benefit of VA loans is that there is no down payment. However, many other great perks come from VA loans, such as unlimited borrowing.

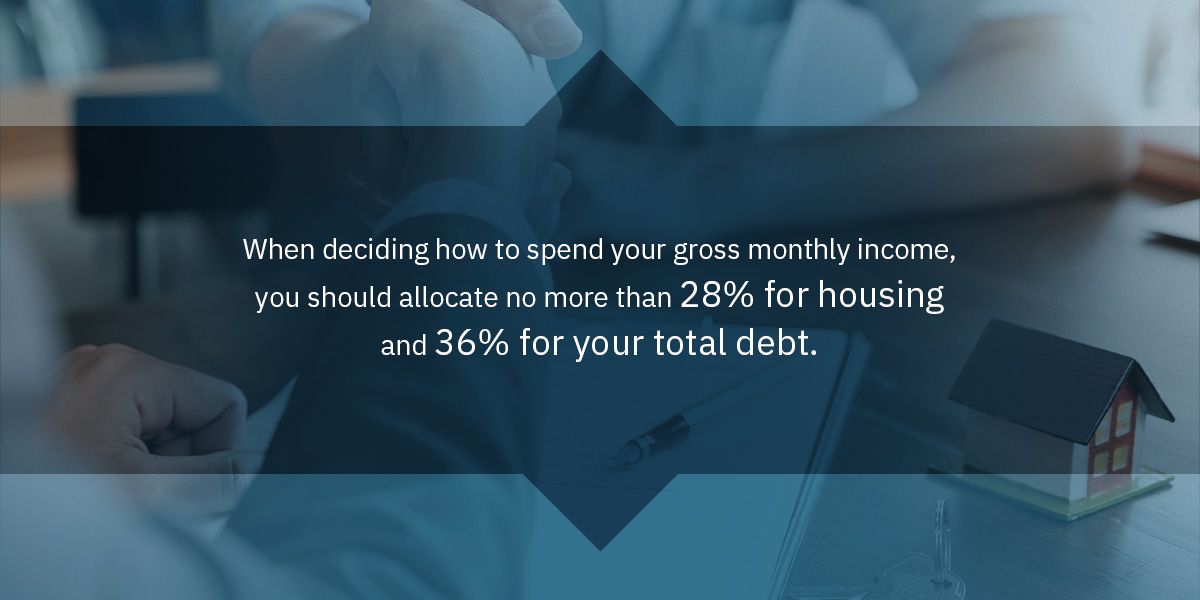

What Is the 28%/36% Rule?

The 28%/36% rule is an important equation that helps with knowing how much house you can afford. It states that when deciding how to spend your gross monthly income, you should allocate no more than 28% for housing and 36% for your total debt. This debt includes everything you owe in a month, such as payments for your student loans, mortgage, credit card, and car. You can use the remaining 64% for expenses such as food and entertainment or put some away in your savings account.

This rule helps you see how much you can afford to pay for a loan each month. While you can make adjustments based on how you want to spend your money, the 28%/36% rule is beneficial when deciding what size loan you can afford.

Most mortgage calculators account for this rule and help you know what kind of house you can afford after you insert pertinent information.

How Does Your Credit Score Impact Affordability?

Your credit score is a major factor when you apply for a loan. Banks use this element to calculate whether you are a risk and how much money they should let you borrow. A higher credit score will enable you to have a lower interest rate, allowing you potentially save hundreds of dollars a month.

Additional factors that affect affordability include your debt amount and how much of a down payment you apply to your house. Having a low DTI ratio and putting down a higher initial payment will assist you with enjoying a lower interest rate, as banks will have greater trust in your ability to pay them back.

How Does the Amount of Your Down Payment Impact How Much House You Can Afford?

You will probably notice that when you put a higher down payment into a “how much house can I afford” calculator, the house will ultimately be more affordable. Putting down a larger down payment on a house affects its affordability in several ways:

- Lowering the loan-to-value (LTV) ratio: An LTV ratio is how much you borrow compared to the value of your home. Having a lower ratio makes lenders more likely to approve your mortgage with reduced interest rates, as they will consider you to be less of a risk.

- Reducing your monthly payments: A large down payment can result in lower monthly payments for a shorter period, as you have already paid for most of the house.

- Requiring you to pay less overall: Lower interest rates help you pay less in the long run due to the larger amount you put down at the beginning.

Learn More About Mortgages From Fort Pitt Capital

If you’re looking for financial advice regarding your mortgage, contact Fort Pitt Capital. Our goal is to do what is best for you.