How to Set Your Child Up for Financial Success

If you search the internet for financial education articles about “money lessons,” there’s list after list of lessons you need to learn by a certain age or rundowns from individuals about what they wish they had learned about money when they were younger.

These financial information catalogs cover everything from saving and investing to compounding interest. Let’s break the cycle of people not learning about money at a young age, and your kids won’t end up writing one of the “what I wish I had learned” lists.

So how exactly should you teach your children about money? The best advice is to start teaching your children about money as soon as possible. Warren Buffet even says to start begin teaching your children these lessons when they’re in preschool. Here’s a breakdown of great ways to incorporate financial education into their lives:

How to Set Your Child Up for Financial Success

Teaching your kids about investing and saving can take many forms. Starting early allows you to integrate essential lessons, so your child can make stronger financial decisions when they are older, whether they are a teenager or a young adult.

1. Offer an Allowance

Setting a weekly allowance for kids in exchange for completing chores can impart an important message that children have to work to earn money. However, this concept can get tricky because you may not want to reward kids for doing chores they should naturally be completing.

A good balance may be having them do normal daily chores but explain that to earn money, they’ll have to do extra tasks like giving the dog a bath. If you give your kids an allowance, don’t take it away as punishment because you don’t want kids to associate money with anxiety. Also, set boundaries so they know what types of things you’ll pay for and what items they’ll have to use their allowance to buy.

2. Help Them to Save

This is where those piggy banks come in and also plays into what I was talking about with setting allowance boundaries. If your child wants to buy that costs more than their weekly allowance, they will have to save their allowance until they have enough money. When putting the money in a piggy bank or jar, kids can physically see the money being saved for a future goal. This helps teach children the concept of delayed gratification.

You can also open a savings account for your kids. Walk them through deposits and withdrawals so they understand how to navigate using a bank account when they are older.

3. Encourage Them to Invest

Open a small investment account and have your children pick a company they like or use. Examples can include Apple, Nintendo, and Mattel. Investing for kids can serve as a powerful lesson because they can learn how the stock market works.

4. Have Them Witness Financial Transactions

Start a savings account for your child and have them participate in the transactions. When completing regular shopping at the grocery store, you might ask your child to count out the cash needed to pay for your food or sort through coupons. You can ask them how much you saved with store cards and deals, encouraging them to find ways to save money in regular shopping and understand sales.

Take your children to the bank and have them fill out the deposit slip. Show them their savings account statements to help them understand how banking works.

5. Provide Ideas for Small Neighborhood Jobs

While allowance is an excellent way for kids to earn their own money, they should understand that there are other work opportunities outside their homes. Many older children and teens run neighborhood businesses providing services for their community. Having a neighborhood business gives them more freedom to choose their hours and work frequency and teaches them that their earnings depend on their schedule, quality, and work ethic.

Some jobs you can encourage your children to take on in your neighborhood include:

- Babysitting

- Lawnmowing

- Raking leaves

- Petsitting and dog walking

Neighborhood jobs can also teach your children about working to meet someone else’s standards and instructions. They might learn how you like to finish tasks, but working for someone else can ensure they strive for quality results that impress neighbors. These habits can develop a strong work ethic that prepares them for the workforce and a successful career.

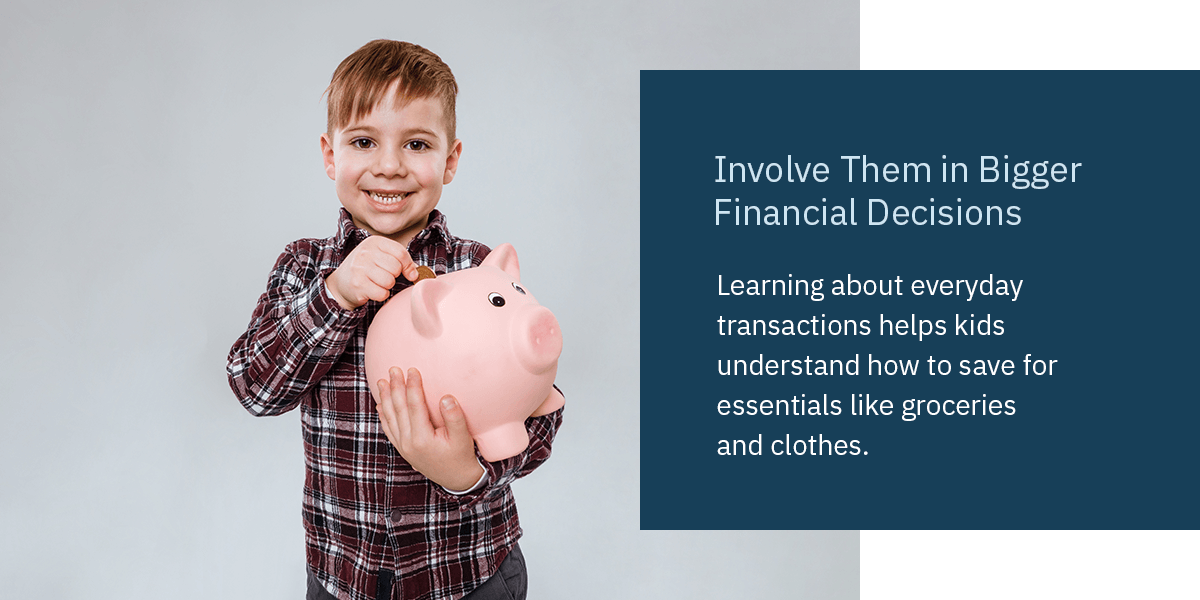

6. Involve Them in Bigger Financial Decisions

Learning about everyday transactions helps kids understand how to save for essentials like groceries and clothes. However, spending often involves larger items and experiences that qualify more as wants than needs. You can help them understand what it takes to save for more expensive things by including them in family spending decisions.

For example, you might want to go on a family vacation. You can include the kids in the planning portion, but take it beyond choosing the destination and activities by asking them to help with the budget. You can give them an amount and have them determine where you can go and what you can do with it.

Another option is to put money in a family fund and let them choose how to spend it when you reach specific amounts. You might take a family tax out of their allowance and put it in the fund to help it grow. Other families put money in from doing good deeds for each other and others.

However you choose to grow your fund, you can check in with the kids to decide how to spend it. They can decide to spend it or wait to do something else at the next touchpoint. This technique can teach them to save over time for something they really want.

The Advantages of Teaching Kids About Investing and Personal Finance

By teaching these essential financial lessons earlier, you set your children up for a lifetime of financial success. However, you can’t just teach these lessons when children are young enough to think a piggy bank is cute. Financial education should continue throughout their adolescence as they work summer jobs, through college, and even into their early 20s as they begin their careers.

Here’s a look at how financial education can change as children age and, get their first jobs, credit cards, and experience more financial firsts:

1. Saving

As kids get older, help them understand the best way to save is to pay yourself first. Meaning, when you get your paycheck, put a portion of it into your savings account first, before you do anything else. Before you pay bills or buy groceries, pay yourself!

Next, they should determine a budget based on the money from each paycheck. After paying themselves first and allocating money for bills and other necessary expenses like food and gas, they will have some money left over to spend on them. This leads us to the next money lesson.

2. Spending

It’s important for kids to consider how they spend their hard-earned dollars. Just because there’s some extra money left over in the budget to spend doesn’t mean you should. Eating dinner out every night or buying a new pair of shoes whenever there’s a sale is not worth it. Is it your Dad’s 60th birthday celebration dinner? Sure, spend the money if you have it. Is it just a regular Tuesday? Maybe make dinner at home and save that extra money.

It’s also vital to learn impulse control. In the moment, your child may really want that new, shiny, sleek watch, but is it really that important? Teach your kids to practice patience before purchasing. They should learn that if they see something they want, they should wait, even for just a day or a week.

It’ll put it into perspective and help your kid see that the thing they “just had to have” isn’t that big of a deal. By waiting and not buying right away, your children will learn to control unnecessary spending, which is critical for successful money management.

3. Credit Cards

While we’re on the topic of spending, let’s talk about one of the significant tools people use to spend their money — credit cards. Kids need to learn the good and bad of credit cards. While using a credit card may seem like “free money” since no cash is exchanged, it’s crucial to remember that credit cards come with a price.

Make sure your children understand they will have to pay that money back to the credit card company and, if they don’t do it on time, they will have to pay interest on top of that. And typically, credit card interest rates are pretty high, so they’ll end up owing much more than they spent. Avoiding credit cards altogether may not be wise, either. Credit cards are a great way to build credit if used responsibly.

Using credit cards responsibly means paying them off in full each month. Here’s a tip — tell your kids to treat a credit card like a debit card. They must have the money in their bank account to pay for everything charged on that card. If there’s not enough money in their account to cover the expense, don’t charge it.

4. Investing

Financial education changes as children get older. Investing will be much more complicated than simply picking a company they like and buying some stock in it. Investing is a great way to build wealth to help pay for more significant expenses down the road. Simply put, investing is allocating funds somewhere now with the expectation of generating a profit later. However, many parents are unsure how to teach kids about investing.

This profit comes from the magic of compound interest. Compound interest means that the interest you are getting back on your money is for the entire pot of money, even as it grows. So in the first year, if you have $1,000 with 5% interest, you’d make $50. Then the following year, that same 5% interest rate is applied to your new total of $1,050, so you’ll make more in interest as your total amount of money grows from that interest.

Your kids will probably like the sound of making more money. It sounds great to be able to make money by simply investing, but caution your children only to invest once they know they can pay their monthly bills and contribute to their savings. It’s also important that they know they’ll want to have saved at least three months’ worth of living expenses in an emergency fund before investing.

So how much should someone invest? A common piece of advice is to invest 10% to 15% of your earnings a year, but if that’s not realistic for your kids, tell them to at least start with the minimum initial investment. No one needs millions or even thousands to invest — you can invest in the market with just a few hundred dollars.

Invest in Your Child’s Financial Future With Fort Pitt Capital Group

When you want to implement strategies to secure your child’s financial future, financial advisory services from Fort Pitt Capital Group can help you reach your personal goals. From saving to investing, we can advise you on how to accomplish your desired outcomes and navigate various financial decisions. You can learn skills to teach your child or set aside accounts ready for them when they reach adulthood.

Contact Fort Pitt Capital Group today to get started.