Creating a Multigenerational Wealth Preservation Strategy

Generational wealth lifts huge financial burdens and offers future generations resources and opportunities they otherwise might not have had. If large enough, it can even support your grandchildren’s needs. However, passing on large amounts of money or assets takes strategy. You must consider your purpose and goals, your family’s financial literacy, and potential tax implications.

Multigenerational wealth planning lets you gift inheritance most cost-effectively. It also protects your family values, regardless of the generation that handles your wealth. This article details what you need to do to protect your assets in the long term.

What Is the 3 Generational Rule for Wealth?

The three-generational rule, or three-generational curse, states that multigenerational wealth dissipates by the third generation. Studies show that about 60% of families exhaust their inheritance by the second generation, while 90% is depleted by the third. This is typically due to a lack of planning, poor investments, and inflation. Focusing on proactive wealth management can help your family be an exception to the rule. Working with a trusted financial advisor can help.

With the Great Wealth Transfer underway, it’s essential to prioritize family wealth management. In the U.S., baby boomers, who are now 61 to 79 years old, control 51.8% of the country’s wealth. By 2045, experts expect spouses and descendants to inherit $68 trillion to $84 trillion. A wealth preservation strategy ensures your hard-earned money stays intact for future generations.

Wealth Preservation Strategies: How to Preserve Generational Wealth?

Wealth preservation plans protect assets from large taxes, investment losses, creditors, and mismanagement. They safeguard retirement funds, identify recipients or beneficiaries, and determine how to hand over assets. You can update your plan as needed, but it should always start with clear and open communication.

1. Have an Open Communication With Your Family

Money conversations improve your family’s financial awareness, values, and skills. If children inherit large sums of money without knowing how to handle it, it can lead to mismanaged finances. While some parents have underlying fears, such as spoiling or demotivating their children once they learn about their inheritance, open communication is more likely to improve trust and manage expectations.

Family governance is the practice of making informed family decisions. This norm alleviates a “shirtsleeves to shirtsleeves” situation — an adage that refers to the three-generational curse. When you talk about family finances, whether in the kitchen or home office, you should involve the next generation in the conversation. Family policies also limit emotionally charged family decisions.

Additionally, your wealth preservation strategy depends on your long-term goals and family values. Some families pursue philanthropy to express such values, while others use trusts to encourage accountability. You have many options for your gifting strategy. You don’t have to fall into a “gift everything or gift nothing” mindset.

2. Set up Trusts

Age, emotional maturity, and financial literacy affect someone’s readiness to receive your gifts. Recipients have complete control over inherited assets through distributions. However, trusts offer a level of protection and control depending on their structure. Types of trusts include revocable and irrevocable trusts, which means:

- Revocable trusts:Also known as a revocable living trust, a revocable trust lets you transfer assets out of your name into your trust’s name within your lifetime. You can add and remove assets, change terms and beneficiaries, and terminate the trust to take back full asset ownership.

- Irrevocable trusts: You permanently give up your asset ownership and control in an irrevocable trust. This protects your assets from creditors, reduces estate taxes, and lets you gift assets in personalized ways. A revocable trust becomes an irrevocable trust after your death.

An irrevocable trust is a structured way to pass down your assets. For instance, it can let you gift funds to your grandchildren but restrict the use to paying college tuition. Generation-skipping irrevocable trusts also skip generations, which offer tax benefits. Examples of irrevocable trusts include:

- Irrevocable life insurance trust (ILIT)

- Spousal lifetime access trust (SLAT)

- Charitable remainder trust (CRT)

- Qualified personal residence trust (QPRT)

- Medicaid trust

- Special needs trust

3. Draft a Comprehensive Will

Estate planning involves long-term planning for passing down your wealth to the next generations. While trusts fall under this plan, you can also draft a will, depending on your goals. A valid, comprehensive will ensures your wealth is distributed appropriately. It can also reduce disputes, which impact your family dynamics.

You should appoint an executor, who can be a family member or a professional. The executor will manage and distribute your assets accordingly.

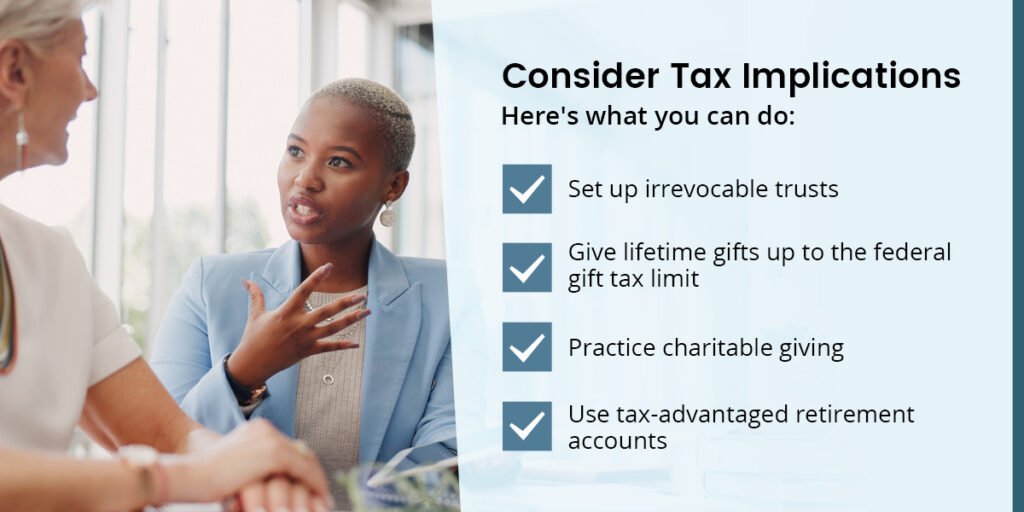

4. Consider Tax Implications

Taxes, like gift tax and estate tax, reduce inheritance value. Tax planning ensures your family receive the optimum value of your assets. Here’s what you can do:

- Set up irrevocable trusts: Irrevocable trusts remove assets from your name, reducing the assets in your estate. This reduces your estate tax, which increases your chances of qualifying for the federal estate tax exemption. The exemption for 2025 is $13.99 million. Due to the reconciliation bill, it will be permanently increased to $15 million in 2026.

- Give lifetime gifts up to the federal gift tax limit:You can offer gifts to your family for up to a specified amount without being taxed. The gift tax exclusion for 2025 is $19,000.

- Practice charitable giving: Charitable donations reduce your taxable income if made toward qualified organizations. These include religious organizations, nonprofit volunteer fire companies, and domestic fraternal societies.

- Use tax-advantaged retirement accounts: Tax-advantaged retirement accounts, like individual retirement arrangements (IRAs) and health savings accounts (HSAs), are optimized for your taxes in the long term. Depending on your IRA type, your contributions may be tax-deductible or tax-free. HSAs also offer triple-tax advantages, where you get tax-deductible contributions, tax-deferred interests, and tax-free withdrawals, provided you follow the terms.

5. Plan for Business Succession

A family business offers multigenerational income if managed and transferred properly. You must have clear succession plans set up years before you retire. You can pass on your business by:

- Gifting your company.

- Setting up an employee stock ownership plan (ESOP).

- Selling your company to your family members.

- Passing the company through a trust.

An ESOP is ideal if your family members are your employees. An ESOP trust lets you gradually sell shares to your family members.

Why Trust Us

Our advisors have been helping clients improve their financial situations since 1995. We offer services best suited to our clients’ needs, operating with a strong sense of integrity and personal responsibility. We believe in transparency and clear communication. We don’t work with product biases and conflicting motivations.

As a fiduciary advisor, we are legally obligated to put our clients’ interests first. Whether you need personal financial services, business investment advice, or retirement plan sponsors, our dedicated advisory team can help you. We’re an SEC-registered investment advisor (RIA), so you can trust our services.

Strategize for Generational Wealth With Our Financial Advisors

Multigenerational wealth is possible with the right strategy. To avoid the three-generational rule, you must have open conversations with your family and teach them the right financial skills. Estate planning is also essential. A trusted advisor can map out your goals.

Whether you need to prepare for retirement or pass on your hard-earned assets, our dedicated and experienced team can help. We can also monitor your goals and make adjustments as needed. Schedule a consultation today to get started.

Disclosures

Kovitz Investment Group Partners, LLC D/B/A Fort Pitt Capital Group is an investment adviser registered with the Securities Exchange Commission under the Investment Advisers Act of 1940 that provides investment management services to individual and institutional clients. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

The information included herein may contain statements related to future events or developments that may constitute forward-looking statements. These statements may be in the form of financial projections and may be identified by words such as “expectation”. “anticipate”, “could”, “estimate”, “will”, “should” or similar terms. Such statements are based on the current expectations and certain assumptions of the author and are, therefore, subject to certain risks and uncertainties.

The description of products, services, and performance results of Fort Pitt Capital Group contained herein is not an offering or a solicitation of any kind. Past performance is not an indication of future results. Securities investments are subject to risk and may lose value.