How to Save for College

Putting a child through college can be a financial burden for many families. Many college students take out loans to pay for higher education, and in some cases, it can take a lifetime to pay it all back. So, how can you help your child save for college? If you do your research, it’s much easier than you may think. Use this guide to start learning how you can save for college.

When Should You Start Saving for College?

While it’s never too early to start saving for college, it’s wise to have a few things sorted out first. While it may feel selfish, take care of your future before saving for your child’s.

To start, create an emergency fund and keep adding to it. You can tap into these savings if you need to pay hospital bills or fix home or car damage. At the same time, work on paying off your debt before saving for your child’s college fund. The sooner you pay off your debt, the more you’ll be able to afford to help your child save money.

Before saving for college, the third thing you should invest in is your retirement plan to ensure you’ll be financially stable after you retire. If you feel selfish about taking care of yourself first, think about it like this — you can always borrow money for college, but you can’t borrow money for retirement. However, if you have enough money when you retire, you can help your child repay their loans.

There’s no wrong way to save for college. You can start whenever you’re ready, but the earlier you start, the greater your chance is to save more. The secret is to remember your needs and future matter, too.

7 Types of College Savings Funds

When starting a college fund, you have several options for savings accounts, each of which comes with unique pros and cons. Some have restricted eligibility or limits on how much money you can contribute per year. Understanding how each type of account could help you save is the first step in starting a college fund. Let’s take a closer look at some commonly used college fund options.

1. Education Savings Account

An educational savings account (ESA) is like a Roth IRA, except it’s only for education purposes. ESA accounts are beneficial because they grow tax-free. You can withdraw the funds without taxes to pay for college and other education expenses like K-12 private school tuition, vocational school, school supplies, textbooks, or tutoring.

The benefits of an ESA include:

- The account is tax-deferred.

- You can transfer it to the beneficiary’s relative who is under age 30.

- There’s flexibility in terms of where you can spend the money.

The disadvantages include:

- You can only contribute up to $2,000 a year until the beneficiary turns 18.

- The beneficiary must use the money in the account by age 30.

- There are income restrictions on who can contribute to an ESA.

2. 529 Plan

A 529 plan is another way to save money for college with tax benefits. Since states sponsor 529 plans, their structure varies by state. As a result, you can use a plan in a different state than the one you live in, and further, you can apply the plan to a school in a separate state than the one where you opened it. For example, if you live in Pennsylvania, you can contribute to a plan in Montana and apply the funds to a college in Arizona.

Benefits of a 529 plan include:

- As the owner, you have complete control over the funds so that you can use the money for its intended purpose.

- There are no income restrictions limiting eligibility.

- You can contribute higher amounts of money to this account.

- The money can sit as long as you like — you don’t need to withdraw it by a specific age.

Disadvantages to a 529 plan include:

- Some 529 plans change your investment options based on your child’s age.

- There is limited flexibility.

- A 529 plan can affect how much financial aid your child receives.

3. Prepaid 529 Plans

Outside ESA accounts and 529 plans, you may want to consider other choices. Doing extensive research before investing in anything is essential, as there are many aspects to learn. No single option is the best — it’s all about finding what will work best for you and your family’s needs.

For the most part, prepaid 529 plans follow the same rules and restrictions as a regular 529 account. As the name suggests, prepaid 529 plans allow you to pay in advance for blocks of tuition at a state university. This strategy lets you lock in today’s tuition rates, which could give you a significant discount since college tuition rates are subject to increase.

While these plans could save you money, you should read the fine print before choosing a prepaid 529 plan. Prepaid tuition plans can be challenging to understand. They can differ in every state — some may restrict how you can spend the money or have rules regarding your child’s acceptance to the school. A significant disadvantage of prepaid 529 plans is that they’ll often only cover tuition and fees, which means you’d have to pay for room and board.

Benefits of a prepaid 529 plan include:

- You can counteract rising tuition by paying for today’s rate.

- The rules of a regular 529 apply.

Disadvantages to a prepaid 529 plan include:

- Only some states offer these plan types.

- The program often limits your child to schools in your state.

- It might not cover expenses other than tuition, like room and board or textbooks.

4. Roth IRA

While most people use Roth IRA accounts to save for retirement, some financial planners also suggest saving college money in these accounts. Doing so can be beneficial because the money will grow and is available for tax-free withdrawal. Plus, if your child ends up not needing the funds, they’re still there for you. Understanding how to use Roth IRA funds to pay for higher education expenses is critical.

Unlike the 529 plan, the existence of a Roth IRA account won’t affect your child’s financial aid. However, withdrawing the money can harm the potential for financial aid because it increases your income. If possible, it’s a good idea to wait until your child graduates, then use the Roth IRA contributions to pay off their student debt.

Benefits of a Roth IRA include:

- You have more freedom to use funds, making it a great option if your child decides to forgo a college education or doesn’t have student loans to repay.

- Having this kind of account still allows for financial aid options.

Disadvantages to a Roth IRA include:

- Withdrawing funds counts as increasing your income, changing your child’s eligibility for financial aid.

- You will have limits on how much money you can contribute each year.

- You can only contribute your post-tax income.

5. Brokerage Accounts

A brokerage account is a regular investment account that offers much flexibility in saving your money. You can contribute as much money as you’d like, and you can withdraw any amount at any time without penalties. Crucially, you can use the money for whatever you want, whenever you need it.

The downfall of brokerage accounts is that they don’t include any tax breaks. Although tax-deferred accounts like the ESA and 529 can provide significant savings, you might be losing out on the flexibility of options within brokerage accounts.

Benefits of a brokerage account include:

- It is easy to establish and start.

- You have a wide selection of investment options.

- You have higher security on your investments than other account types.

Disadvantages to a brokerage account include:

- Brokerage accounts are riskier, and return on investment is not a guarantee.

- Market conditions are constantly shifting, so you will need to monitor changes.

- If you want an advisor, you might have to pay a fee.

6. Uniform Transfer/Gift to Minors Act

We only recommend Uniform Transfer to Minors Act (UTMA) or Universal Gifts to Minors Act (UGMA) plans as a last resort. If you didn’t qualify for any other college savings account, consider a UTMA or UGMA plan. While you’ll set up one of these accounts in your child’s name, you’ll control it until the child is 18 for a UGMA plan or 21 for a UTMA plan. Once your child is old enough, they’ll be able to spend the money however they choose.

Like the 529 and ESA plans, UTMAs and UGMAs have tax advantages. The most significant downfall of this choice is that there’s no guarantee that the recipient will use the money for college expenses. Because your child is free to use the money for whatever they like, they may decide to use it to pay for something other than college.

Benefits of a uniform transfer include:

- These plans are great supplementary or alternative options to other savings plans like an ESA or 529.

- Your child can use them for whatever they would like once they get control over the account, giving them options outside of a college education.

- You will pay a lower tax rate on collected funds.

Disadvantages to a uniform transfer include:

- You must keep the same beneficiary until your child reaches the determined age.

- While taxes are lower, other options have no taxation.

- Your child might use funds irresponsibly after gaining control of the account.

7. Regular Savings Accounts

While there are many types of funds designed to help yield high growth and support your child through college, a simple savings account can also be a powerful resource. You can select the type of savings account you want to open, allowing you to choose the interest rates and access level. Since you will manage the account, you can develop a more personalized savings plan to create funds for your child.

Benefits of a savings account include:

- You can change the purpose of this account later, making it perfect if your child chooses an alternative path to college.

- There are no restrictions on money use or application.

- They make great supplementary accounts to other savings initiatives for additional funds.

Disadvantages to a savings account include:

- You are entirely responsible for making deposits and sticking to your payment plan.

- Low interest rates can make growth slow.

- No restrictions prevent a beneficiary from using the money before your child goes to college.

How Much Should You Save for College?

Often, the amount you will need to put aside for your child’s college education will depend on the institution they want to attend. Each college option has vast price differences. In 2022, attending college in the U.S. costs an average of $35,331 per year. This cost includes tuition, textbooks, and other fees.

However, several factors can impact college costs. You might have to pay additional fees depending on where your child goes to school.

While in-state tuition averages just over $9,300, out-of-state rises to over $27,000. You will need different savings strategies to afford out-of-state tuition for your child over in-state. Each state also has varying tuition rates, where some states raise higher than others.

As you begin to budget and plan for your child’s college fund, you should research the average cost of college in your state to get a more accurate representation of your savings goals. Vermont had one of the highest public in-state tuition rates in 2021, costing students around $16,600 annually. On the other hand, Florida only costs around $4,400 each year for a public in-state school.

Additionally, you should consider public versus private schools. Private colleges can average over $35,000 annually for tuition alone — total fees for a private college can easily cost over $50,000 each year. While many families prefer the many perks that a private university education can offer, you will have to save accordingly to ensure you can afford the fees.

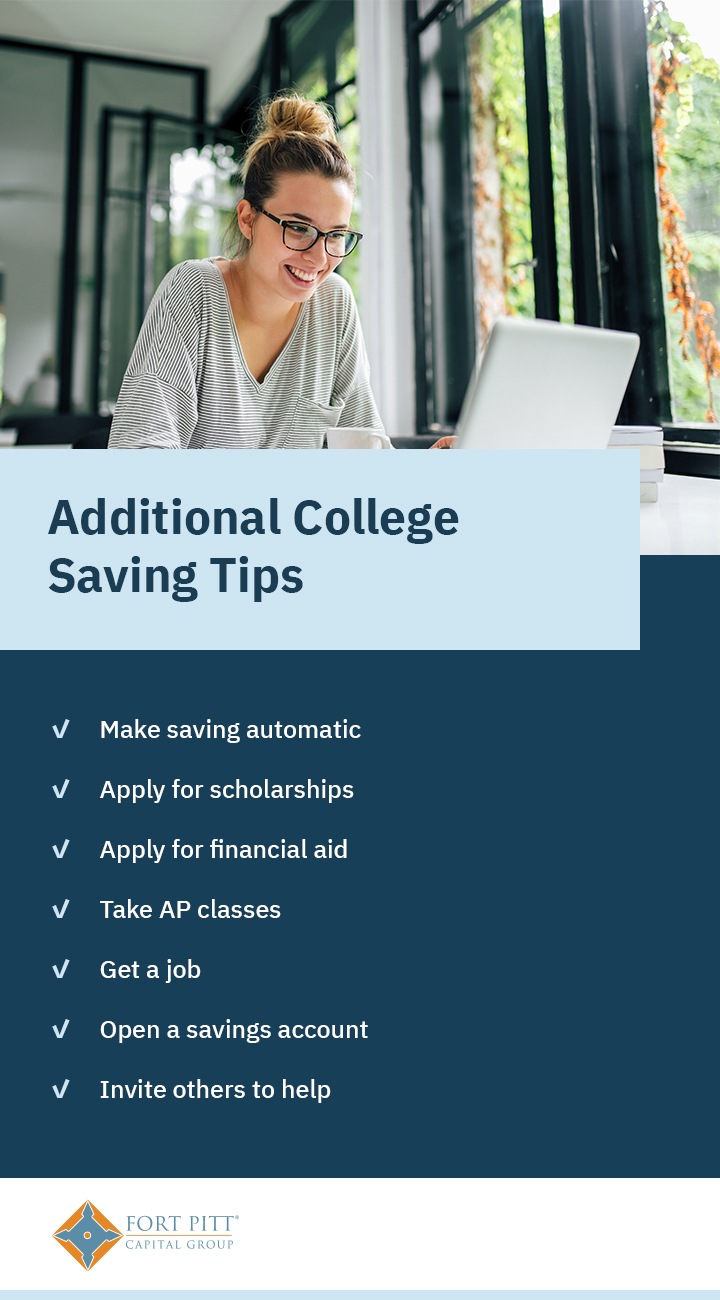

7 College Saving Tips

Long-term saving for college is more than setting up savings accounts and making contributions. To maximize your child’s education savings, consider these additional tips.

1. Make Saving Automatic

Once you create or designate an account for college savings, set up your checking account to automatically transfer a specified amount into your college account. Make sure you choose an amount that you can manage without putting yourself in challenging financial straits. Automatic contributions require less thought, and when you don’t have to check on them every time you contribute, it’ll make the savings seem like they’re growing faster.

2. Apply for Scholarships

Scholarships are incredibly beneficial, and you can get them for various reasons. Typically, students who excel in academics, sports, or extracurricular activities can qualify for scholarships. Your child should apply to all scholarships for which they’re eligible. It’s free money that you don’t have to pay back. Even small scholarships can add up and save you money.

3. Apply for Financial Aid

Another way to receive free money for college is through the Free Application for Federal Student Aid. Schools use this form to determine how much money they can offer in the form of school aid, state aid, work-study positions, and federal grants. FAFSA also provides student loans, so make sure you know what you’re accepting.

4. Take AP Classes

Your child can take advanced placement classes in high school. For each AP course exam your child passes, they can earn college credits, which means fewer classes you’ll have to pay for. Some high schools even provide students with the option to take courses from a local community college while in high school, which is another excellent way to earn transferable credits and save money in the future.

5. Get a Job

Encourage your child to get a job. Whether it’s a part-time position during the school year or a full-time summer position, working is a great way to earn and save money. A job is also beneficial because your child will gain experience to add to their resume for college applications and future job applications.

6. Open a Savings Account

As your child earns money, they’ll need a safe place to save it. Help your child set up and contribute to a savings account. Many banks offer accounts designed specifically for students, which are typically more lenient about minimum balance requirements and offer waived fees. Having a savings account can also help teach your child responsibilities and the value of saving.

7. Invite Others to Help

Another way to add to your college accounts is to involve your friends and family. Invite family members to make contributions as a holiday or birthday present. Some accounts, like 529s, include ways to accept contribution gifts or offer account-specific contribution gift cards. Remember that gift contributions can be small amounts, and they’ll still be helpful. Every little bit helps!

College Savings FAQ

If you’re searching for answers to additional questions, consider speaking with an experienced financial advisor.

Should I Save for Retirement or College?

Generally, it’s a good idea to make sure you have yourself taken care of first. Financially taking care of yourself in retirement will lessen the burden on your children. If you have your heart set on saving for both simultaneously, it’s crucial to find a balance between saving for college and saving for retirement. Consider testing the saving rates for each and how you can adjust them to grow both accounts.

How Much Should I Be Saving?

How much money you save will ultimately depend on what you can afford and when you start saving. First, determine what percentage of the cost you want to pay for. You can research the cost of an in-state public college and use that number as a baseline. To start, consider saving one-third of the cost of a public college in your home state. Aim to pay a third out of pocket during your child’s attendance and finance the rest through loans.

Of course, if you want to save more or less, adjust the strategy to work with your goals.

What Happens to a 529 if My Child Does Not Go to College?

If you create a 529 plan for your child and they decide not to go to college, you still have options. The money in this account can sit indefinitely, so there’s no rush to take it out. If your child chooses to go to a trade or vocational school, you can apply money growing in a 529 account to those schools as well. If it turns out your child doesn’t need the money, you can always change the beneficiary to another family member at any time.

What Is the Best Account to Save for College?

The most common accounts used to save for college are ESAs and 529 plans. Ultimately, the best choice will depend on your family’s needs. The most effective way to determine what you need is to meet with a financial advisor.

How Do I Start Saving While My Child Is in High School?

If your child is older, you still have options to help them save:

- Start a Roth IRA: Roth IRA accounts are great ways to retroactively pay for college tuition and fees because you can use them to pay for any student loans you or your child take out while studying. This option gives many families the flexibility to save while sending their children to the school of their choice.

- Open a 529 plan: You can also open a 529 plan at any time in your child’s life. While there might be some risks involved, it is a great way to save up some money to support your child’s college education while they are in high school.

- Encourage them to take AP classes: AP classes and grades are another way to help cut costs while your child is preparing for college. Good AP test scores can help your child test out of one or multiple required college courses, reducing the number of classes you need to pay for. They might even be able to graduate early.

- Help them seek scholarships: High school grades and practice SAT (PSAT) scores can help your child qualify for scholarships from their target schools and national organizations. Research potential scholarships and encourage your child to maintain the grades they’ll need to earn them.

Professional consultation can help you find and understand all your choices. Set up a meeting with a reputable investment advisor to investigate your options.

Talk With an Advisor

Knowing the ins and outs of all your college savings choices can be overwhelming. Talk with a financial advisor at Fort Pitt Capital Group to create a plan to save for college. Our experienced advisors will provide guidance even after your plan is in place. Contact us today to learn how we can help you with your investment goals.